The payments space is experiencing a lot of change.The pandemic's influence over how retailers and consumers think about payment channels is still present today.

The buy now, pay later model has been on the rise, and with it, concerns over consumer debt levels as more shoppers take on payment plans for everyday purchases. The advantages of checkout-free capabilities are still being tested, as retailers pursue convenience in new store concepts. And retail giants like Walmart and Amazon are introducing new payment offerings and pursuing deeper efforts in the space as consumers' preferred payment options change.

AI has complicated things further, introducing new checkout experiences and shopping settings. Retailers are thinking through the best way to streamline and incorporate payment options as a way to capture, delight and retain shoppers.

As the space shifts, the future of who will best utilize and employ new means of supporting retail operations through different payments is anyone's for the taking.

Agentic robots that shop and pay without human involvement could render marketplaces obsolete – and major retailers are responding.

By: Justin Bachman• Published Feb. 11, 2026

Retail marketplaces like Amazon and eBay face a quandary when it comes to artificial intelligence shopping robots roaming their enormous digital bazaars, which were designed for humans.

Merchants pay fees to access these sites’ huge pools of shoppers and for a variety of other services, such as shipping, logistics, payment support, product returns, marketing assistance and selling tools. Over time, consumer shopping agents are expected to move from product research — with humans still completing the payment — to fully autonomous, end-to-end transactions.

For marketplaces like Amazon and eBay, the large language models that are moving swiftly into agentic commerce – including Perplexity AI, OpenAI and Google – are potentially disruptive to their model, said Adam Behrens, the CEO of New Generation. The San Francisco-based software startup builds agentic commerce tools for merchants. (The company’s parent is Internet Forest.)

“You can look at what ChatGPT and Google are trying to do as kind of like opening the doors for an LLM to act as the marketplace where, if you just connect supply into that language model and then a consumer interacts with it, why do you ever need to go to Amazon?” Behrens, a former Stripe executive, said in an interview.

In that model, the traditional e-commerce marketplace “just becomes the back-end fulfillment,” he added.

The marketplaces aren’t sitting still.

EBay has updated its user agreement, effective Feb. 20, to block any agentic commerce tools, including “buy-for-me agents, LLM-driven bots, or any end-to-end flow that attempts to place orders without human review” without the company’s permission.

That update aims to “keep interactions predictable and safe, so we can protect buyers and sellers, apply appropriate safeguard and usage limits, and maintain a reliable experience,” an eBay spokesperson said in an email.

Other merchants are also likely to view agentic commerce warily.

The technology poses a potential double-edged threat: Erosion of a customer relationship and the potential for increased fraud on the transaction side if they “effectively outsource” payment-trust decisions to systems outside their control, said Jeff Otto, the chief marketing officer of New York-based Riskified, which sells merchants software to manage fraud and chargebacks.

“You’re kind of losing on both sides, your brand exposure, loyalty, all those things that create customer lifetime value – you lose all that when it's inside of a ChatGPT interface, and then second, you’re taking on this risk,” Otto said in an interview.

The change comes as the San Jose, California-based marketplace has piloted its own “in-house” LLMs to facilitate commerce, Chief Executive Jamie Iannone said during the company’s earnings call in October. “We’re now poised to gradually bring agentic capabilities into the core of eBay’s business through the main search experience over the coming quarters,” he said.

That new platform “enables a fully connected experience via eBay agents and third-party agents like OpenAI in real-time,” Iannone added.

EBay is working with partners to make its inventory available to third-party agents that understand “eBay’s valued-added services,” such as managed shipping and money-back guarantees, the spokesperson said. The company’s goal is “to maintain eBay's unique value proposition within agent-to-agent interactions.”

In November, Amazon sued Perplexity AI in federal court in San Francisco, seeking an injunction to stop the AI firm’s agentic shopping tool, Comet, from accessing the retail store and customer data. Amazon is also driving consumers to Rufus, its AI shopping assistant.

“No different than any other intruder, Perplexity is not allowed to go where it has been expressly told it cannot; that Perplexity’s trespass involves code rather than a lockpick makes it no less unlawful,” Amazon wrote in its complaint, alleging violations of U.S. and federal computer fraud and abuse laws.

According to the retailer, its store “is more than a catalog of webpages: it is an integrated, dynamic environment that provides Amazon customers with a secure, curated, and individualized shopping experience.”

In a cease-and-desist letter to Perplexity days before its lawsuit, Amazon said it “shares the industry’s excitement about AI innovations and sees significant potential for agentic AI to improve customer experiences in a range of areas.”

However, it added, AI agents must operate “transparently” as this “protects a service provider’s right to monitor AI agents and restrict conduct that degrades the customer shopping experience, erodes customer trust, and creates security risks.”

Merchants – whether it’s an Amazon-sized emporium or an individual entrepreneur in a rural village – are navigating how to best approach agentic commerce.

“The imperative for a merchant becomes: How am I going to expose my brand, my data, my products, to this ecosystem in a way that I maintain some level of control, that I still benefit from it, that it translates to real revenue?” Behrens said.

Article top image credit: Getty Images

Amazon to halt palm payments

The company said all Amazon One palm readers will be removed from physical stores by June 3.

By: Patrick Cooley• Published Jan. 30, 2026

Amazon said it is shutting down its Amazon One tech payment tool, which lets customers pay by scanning their palm at some physical Amazon stores, along with other businesses such as the restaurant chain Panera Bread.

All Amazon One palm readers will be removed by June 3, although some stores may remove them earlier, an undated FAQ page on Amazon's website says. The discontinuation is a “response to limited customer adoption,” an Amazon spokesperson said in an emailed statement.

The announcement, which the company made on its website, comes as Amazon said it would shut down all of its Amazon Go and Amazon Fresh stores. The spokesperson said messages were sent to Amazon One users about the discontinuation on Jan. 27. The Amazon Fresh and Amazon Go stores will close on Feb. 1, the spokesperson said, with the exception of some California locations.

The Amazon One devices let customers check in at Amazon stores and pay at checkout with the scan of a palm as long as they signed up for the service and entered their payment information ahead of time.

The palm readers were first introduced at two Seattle Amazon Go stores in 2020, and were eventually introduced at other Amazon properties such as Whole Foods.

All data associated with the palm readers will be deleted “following the discontinuation of the services and after completion of any remaining transactions,” the company said on the web page announcing the discontinuation.

Amazon Go stores have employed so-called cashierless checkout, in which a customer scans a credit card or other payment method when they enter a store and a system of cameras tracks what they take off the shelves and charges them for it.

The online retailer already dropped its cashierless “Just Walk Out” technology at its own grocery stores in 2024, although the technology remains in some third-party stores.

The company did not explain why Amazon Fresh and Amazon Go stores are being shuttered, but said in a statement that an unspecified number of those stores would be converted to Whole Foods.

Cashierless checkout has advanced in fits and starts in recent years, and experienced a major setback when the company Grabango, which provided the cashierless systems to retailers, went out of business in 2024.

However, analysts and consultants who follow the industry are confident that businesses will eventually be able to make cashierless checkout work at a larger scale as the underlying technology that powers it advances.

Article top image credit: Courtesy of Amazon Web Services

Walmart alumni open POS test lab

As retailers seek omnichannel sales solutions, a new vendor-neutral demonstration lab offers point-of-sale equipment evaluation.

By: Justin Bachman• Published April 9, 2026

As retailers seek point-of-sale systems to integrate various sales channels, a retail technology firm founded by Walmart technology alums has created a demonstration lab that allows merchants to test multiple POS vendors’ wares.

Kitestring Technical Services aims for its innovation laboratory to be a vendor-neutral testing and demonstration site for retailers to evaluate POS equipment in the market. The lab currently has seven software and 14 hardware vendors.

Point-of-sale equipment decisions are major, multiyear, multimillion-dollar projects for retailers, carrying multiple risks across hardware and software choices, said Lindsay Schwab, Kitestring’s head of partnerships and growth. As a result, such decisions are generally made with extreme caution.

“We like the idea of being able to have retailers come into our office and be able to see, side by side, all of the different point-of-sale systems that they’re interested in,” she said in an interview from Kitestring’s lab in Bentonville, Arkansas.

Kitestring debuted the lab in January at the National Retail Federation’s annual Big Show conference in New York City.

Kitestring is a privately held, family-owned company, with about 140 employees, led by CEO Jared Smith who acquired the business from his father, Larry Smith. The company has evolved from point-of-sale work that many of the current management team performed for retail giant Walmart over the past 20 years, Schwab said.

Today, Walmart and its Sam’s Club wholesale operation account for only about 20% of Kitestring’s revenues, Schwab said. The diversified company now counts major grocers, department stores and a half dozen major convenience store chains as clients as well. Kitestring’s customers generally have annual sales above $300 million, she said.

Many retailers want integrated solutions to handle sales in various points: Digital, in-store, kiosk, mobile and orders from third-party retail sites like DoorDash and Uber Eats, said Justin Clark, retail technology specialist at Kitestring.

“If you’re going out there on the market today, you’re looking for a modern architecture that can do the online, along with the in-store experience as well,” he said in an interview.

The POS market has become more “agnostic” in terms of mixing hardware and software solutions from various providers, as long as the systems are designed to run on the same operating system such as Android, Linux or Windows, Clark said.

One of Kitestring’s customers, Altaine, a digital commerce technology firm, has used the lab to show a prospective retail client how its software handles an order flow with actual hardware, Jo Gelb, Altaine’s co-founder and chief operating officer, said in the call with Schwab and Clark.

“Obviously, everyone can do an emulator demo and just show screens, but what I think is quite powerful is to be able to show the emulator alongside the physical bits of hardware,” she said. Altaine’s order platform is used by merchants that include BP, Pizza Hut and Subway.

When Altaine lands a prospective customer, it turns to the laboratory for product demonstrations “because we know that they actually are nearly as expert on our technology as we are, just because of the hands-on nature of putting it in a lab,” Gelb said.

Diebold Nixdorf, a major supplier of POS and ATM products based in North Canton, Ohio, has implemented its retail hardware and software solutions at the lab.

“Retailers can experience how their POS and omnichannel solutions perform in realistic store scenarios and figure out how seamless retail experiences and personalized interactions can look,” Ed McCabe, Diebold Nixdorf’s head of retail sales for North America, said in an emailed company statement.

Article top image credit: Getty Images

Digital wallet use outpaces regulators

Consumers are increasingly turning to these mobile tools for convenience and new features, and regulators are trying to catch up.

By: Justin Bachman• Published Dec. 8, 2025

Back in 1999, eight years before Apple’s first iPhone release, a Silicon Valley software startup named Confinity introduced what it called a new “killer app.” It was dubbed PayPal.com.

The service allowed the “beaming” of funds between users, with only an email address. “Beaming Money by Email is Web’s Next Killer App,” Confinity said in its press release pitch, describing the technology.

The money-by-email effort arose from an earlier Confinity concept to transfer funds using infrared beams. The company demonstrated its payment feat by transferring $3 million with Palm Pilot devices in a breakfast display dubbed “Beaming at Buck’s” in the summer of 1999 at Buck’s, a Woodside, California restaurant. Max Levchin, the startup’s co-founder, recounted the story several years later in a talk at Stanford University with his Confinity co-founder, Peter Thiel.

A quarter century on, what began as a pioneering effort to encrypt money and move it digitally has morphed into a global payments industry anchored at the consumer level with digital wallets worldwide on billions of mobile phones. The mobile wallet has become standard for many consumers, some of whom consider a plastic payment card as outdated as a landline phone.

Regulators are still struggling to catch up with financial technology innovators. While the Biden administration tried to impose new oversight on big tech providers of digital wallets and peer-to-peer payments — such as Apple, Google and PayPal Holdings — the Trump administration has reversed that regulatory course.

Ages removed from the era of email payments, today’s digital wallets serve an extensive menu of functions: they now can carry a digital passport and driver’s license; store concert tickets and cryptocurrency; trade stocks; enable lending; allow paycheck deposits; and hold virtual credit and debit cards that can tap rewards currency.

The wallets also, of course, provide payment at physical stores and online. Meanwhile, financial technology companies like Cash App parent Block and PayPal are expanding the wallets’ feature sets to attract new customers.

PayPal leads the mobile wallet pack

Question in third-quarter: Which payment services have you used in the past 12 months?

More than three-quarters of Americans (77%) surveyed used at least one of the three most popular U.S. wallets — PayPal, Cash App and Apple — during the third quarter, according to data from Statista, which surveyed about 60,000 U.S. adults online, ranging in age from 18 to 64.

On average, U.S. consumers made 11 monthly payments with their phones in 2024, compared to four in 2018, the Federal Reserve found in its annual survey of payment methods. “Households earning less than $25,000 per year and adults 55 and older relied more on cash than other cohorts,” the May Fed report said. “In contrast, adults aged 18 to 24 were more likely to pay with a mobile phone, using their phones for 45% of all payments.”

Globally, about 4.5 billion people use a digital wallet today, with the number expected to grow to six billion by 2029, according to a November report from Juniper Research.

Precise U.S. wallet usage figures are difficult to determine. Apple and Google, for example, group their wallet revenue figures within larger categories of sales, such as services and subscriptions, and neither releases user numbers. Block, however, discloses Cash App’s user growth by releasing the number of monthly active users.

The “larger participants” rule

After analyzing the rapid growth of digital wallets, the CFPB in the Biden administration adopted a far more expansive view of what kind of guardrails were necessary for the industry. It followed through with a new rule boosting oversight of big tech companies that offer digital wallets in hopes of better safeguarding users.

Digital wallets are “doing a lot of bank-like activities, but their regulation is different from banks,” Lacey Aaker, a former CFPB policy analyst who worked on the now-defunct rule, said in an interview, noting the bureau’s rationale.

Many people use wallets and feature-rich financial apps as their primary source of banking. They don’t read deeply into companies’ disclosures about which funds may have federal deposit insurance or which debit payments are covered by the Electronic Funds Transfer Act, said Aaker, now a policy analyst with the nonprofit Consumer Reports.

“When we think about the everyday consumer, they don’t have time to read through all of the fine print,” she explained. “They have lives and jobs.”

In November 2023, the CFPB proposed a rule — “Defining Larger Participants of a Market for General-Use Digital Consumer Payment Applications” — to address the perceived problems within the burgeoning financial technology industry.

“Big Tech and other companies operating in consumer finance markets blur the traditional lines that have separated banking and payments from commercial activities,” the bureau said in a press release announcing the rule. The bureau concluded that “this blurring can put consumers at risk, especially when the same traditional banking safeguards, like deposit insurance, may not apply.”

The bureau’s final rule, which was rolled back earlier in 2025, would have extended supervision to seven “nonbank firms” that processed at least 50 million consumer transactions per year or about 98% of the 13.5 billion consumer payment transactions.

The CFPB did not identify any specific companies that would have been covered, nor did it include cryptocurrencies such as stablecoins within the rule. In December 2023, the bureau declined to reveal wallet data to sister publication Payments Dive under a Freedom of Information Act request, citing an exemption in the law for privileged and confidential information.

Nonetheless, the names surfaced in 2025 when Congress moved to reverse the Biden-era CFPB rule. The Congressional Review Act resolution that overturned the regulation cited the seven largest digital wallet providers, namely Google, Apple, Samsung, PayPal and its Venmo unit, Block’s Cash App and Meta’s Facebook.

The goal was “really trying to sort of figure out what is the right amount of regulation for these types of apps and these types of platforms, that has consumer protection that doesn’t stifle innovation,” Aaker said.

Most critically — to the industry’s indignation — the bureau aimed to impose supervisory examinations of nonbank technology behemoths’ operations, much the way regulators oversee banks.

Tech companies and retailers including Apple, Etsy, Google and Netflix vehemently opposed the rule, which took effect in January 2025, weeks before the incoming Donald Trump administration. The tech firms filed a federal lawsuit to block the rule and lobbied lawmakers to rescind it under a congressional resolution, which passed and Trump signed in May.

The rule was a case of the bureau “getting over its skis,” said Jonathan Pompan, a Washington attorney with the law firm Venable, who advises financial services firms.

“It was trying to retrofit legacy consumer credit laws onto modern payment technology,” Pompan said. “And Congress recognized the mismatch and pulled the plug, while at the same time the administration was effectively placing [the CFPB] on life support.”

Protesters gather outside the Consumer Financial Protection Bureau on February 12, 2025, in Washington, D.C. The Trump administration has sought to dismantle the CFPB under Acting Director Russell Vought.

Kent Nishimura via Getty Images

A regulatory smorgasbord

Digital wallets operate under a patchwork of state and federal laws, including their relationships with banks for deposit insurance on customer funds and obligations to consumers under the Electronic Funds Transfer Act and Regulation E, said Laura Huntley, a managing director with FTI Consulting and a former banking regulatory attorney.

Banking regulators, the CFPB and the Federal Trade Commission also monitor financial firms for compliance with unfair, deceptive or abusive acts or practices, known as UDAP laws.

The states monitor money senders under their money transmitter licensing rules, with enforcement powers. Many of the activities within wallets are also monitored by the Treasury Department’s Financial Crimes Enforcement Network for compliance.

Wallet and P2P companies are “highly regulated,” said Miranda Margowsky, a spokesperson for the Financial Technology Association, which counts PayPal and Block as members.

The firms are “directly regulated” by states as licensed money transmitters and their bank partnerships fall under the purview of federal supervision, she said. Wallet companies also are subject to several U.S. consumer protection laws, Margowsky noted.

Despite the death of the CFPB’s larger participant rule, “I don't think we could ever say wallets weren’t really regulated,” Huntley said in an interview. “They have been regulated and will continue to be regulated under exactly the same messy regime.”

“Even if the rule had gone into effect, the existing federal and state frameworks would have remained fully intact,” she added. “What we would have been doing there is just adding another supervisory layer on top of something that’s already pretty dense.”

The bureau under former CFPB Director Rohit Chopra was “so aggressive,” she said. “We’re definitely seeing the pendulum having swung,” in terms of the bureau under Trump, Huntley said. “I think we got to a point there for a second where we said no risk was acceptable. And that’s crazy, because we’re in business.”

Currently, the bureau lists a dozen financial service areas where consumers may lodge a complaint, including with respect to “money transfers, virtual currency and money services.”

Beyond consumer payment services, the CFPB itself is facing critical questions about its future.

In November, the bureau said that the Justice Department had determined its quarterly funding mechanism from the Federal Reserve System was illegal and that its existing budget would lapse by early 2026. The agency also transferred its litigation and other legal enforcement work to the Justice Department, according to multiple media reports, some of which included reporting on plans to furlough most remaining CFPB staff.

Huntley and others pointed to the role that state attorneys general will increasingly play in consumer financial enforcement in the CFPB’s absence.

“I know we’ve been threatening this for a long time, but the states, they are coming,” Huntley said, noting that many former federal regulators at agencies like the CFPB and Office of the Comptroller of the Currency have moved into state roles.

Consumer trust and market policing

Unlike many developing markets such as Brazil, China and India, the U.S. has a long history of debit and credit card use, which in many ways has slowed the development of full-service financial wallets and their regulation, said Raynor de Best, a financial services analyst with the Hamburg, Germany-based market research firm Statista.

Emerging markets “skipped” the credit-and-debit era and designed payments around mobile wallets, said de Best, who studies the digital wallets market. “They wanted to push financial inclusion and they built the (payments) system along with the regulation at the same time,” he said.

Wallets and other payment platforms are deeply invested in safe products and competent customer service because of the financial consequences of shoddy products and trouble for their consumers, said Josh Istas, head of product for The Strawhecker Group, a financial services consulting firm.

“If that trust is abused in any way, shape or form that is against their major objective of growing their platforms,” Istas said. “There’s incentive from reputable good actors to ensure consumer protections.”

Google maintains dialogue with regulators, policymakers and industry partners to promote consumer protections given the growth of digital wallets, a Google Wallet executive, Dong Min Kim, said in an email from the company. Google also believes that the industry needs consistent regulatory frameworks to foster trust and innovation, he said.

Recent changes at Cash App — incorporating digital currencies and lending to a broader group of customers — are meant to respond to customer demands reflecting “how they participate in the modern economy,” Owen Jennings, Block’s business lead, said Nov. 13 during a product release event.

“Cash App is on this journey from what used to be a simple peer-to-peer app into what’s now a full-fledged financial platform that can allow a customer to run their financial life,” Jennings said. “The level of trust that’s required in order to cross that chasm is much higher.”

Apple and Samsung did not respond to several requests for comment; Block, Google and PayPal declined requests for an executive interview.

Block’s Cash App is one of the few wallets that publicly touts its growth, with 58 million active users in September 2025.

Block’s Cash App is one of the few wallets that publicly touts its growth, with 58 million active users in September 2025.

The wallets and apps ecosystem “has evolved to that point where companies who are offering digital banking need to become a bank to really fall into the framework that makes most sense for the service they’re offering,” contended Kyle Rosen, head of Americas for Thunes, a Singapore cross-border software firm with U.S. customers that include MoneyGram International and Western Union.

“The industry generally leads the regulator in terms of what occurs,” Rosen noted. “There’s innovation and then we need to regulate around it.”

Consumers are unaware of details such as the differences between a bank and fintech or which kinds of funds movements are covered by the Electronic Funds Transfer Act, said Tony DeSanctis, a senior director at Cornerstone Advisors, a bank consulting firm.

Some of the larger wallet risks for consumers revolve around which fintechs or neobanks enter the market, DeSanctis said. Ultimately, it will be about how responsibly new players act.

Article top image credit:

Thomas Trutschel/Picture-Alliance/DPA/AP

Amazon targets pop-up retail with upgraded Just Walk Out tech

The latest changes to its RFID-enabled checkout lanes are aimed at making it easier to use in settings like festivals and temporary stores.

By: Tatiana Walk-Morris• Published Jan. 21, 2026

Amazon is going further with its RFID-enabled checkout lanes. The retailer in January announced an upgraded line of RFID checkout lanes, which can be deployed in hours, with the intent to use them for festivals, pop-up shops and other temporary retail locations, according to a company press release.

Improvements include in-lane screens that guide shoppers through the checkout process and display their cart total, as well as automated gates and better cart visibility. In 2025, the company piloted the upgraded checkout lanes at 17 locations, including the Camp Flog Gnaw music festival and a store at the Circuit of the Americas racetrack, the retailer said.

Amazon’s original Just Walk Out system used computer vision to detect items shoppers picked up, but the RFID checkout lanes are better able to track soft items such as clothing and fan gear.

The company began integrating RFID technology into its cashierless checkouts in 2023 to charge customers for shoes, fan gear and other soft goods. At that time, the company partnered with Avery Dennison to roll out the capability.

Amazon is promoting the checkout lanes as a tool to boost sales and reduce theft. So far, the technology has driven a 47% jump in sales per game at Lumen Field in Seattle. Meanwhile, the University of California San Diego saw its retail theft plummet by 83% after rolling out the technology, Amazon said.

“Through continuous innovation and expanding applications, Just Walk Out continues to deliver on the same promise: streamline the shopping experience so people can get back to what matters most,” Amazon said in its release.

Amazon is expanding its Just Walk Out system in fast-paced, temporary retail settings as it pulls back from using the technology in some other retail environments. In 2024, the company opted to remove it from Amazon Fresh stores in the U.S. Instead, the retailer began introducing Dash Carts, which charge customers for their purchases and bypass the checkout line. In a blog post, the company defended its decision to reverse course by highlighting the technology’s performance in smaller settings like sports stadiums, college campuses and hospitals.

Along with the Amazon Fresh stores, the company also realized that the technology didn’t quite fit in its Whole Foods locations. The software works better in amusement parks, stadiums and other fast-paced retail environments, the company said.

Amazon’s Just Walk Out technology is currently being used at 360 third-party locations globally, and 150 new stores will be added in 2026, including at sports venues, healthcare facilities and universities.

Article top image credit: Courtesy of Amazon

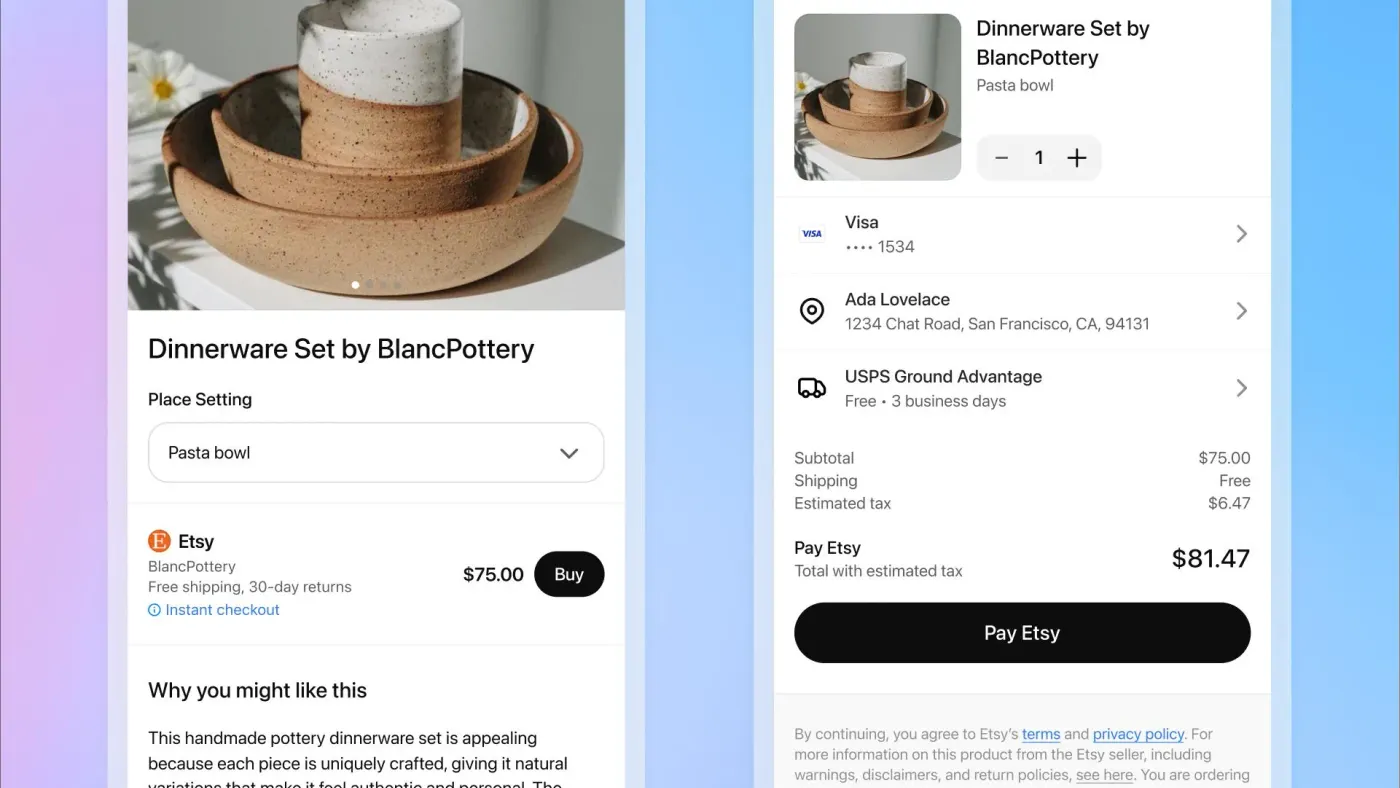

ChatGPT lets shoppers buy products within the platform

Launching first in partnership with Etsy and Shopify, the Instant Checkout functionality has the potential to rival Amazon and Google, one expert said.

By: Dani James• Published Sept. 30, 2025

As consumers turn to AI for shopping recommendations, OpenAI just announced a function that aims to keep the buying process on its ChatGPT platform.

The company in September debuted Instant Checkout for U.S. ChatGPT Plus, Pro and Free users. Such users can now buy directly in the platform from U.S. Etsy sellers and will soon have the same option for over a million Shopify merchants (including Glossier, Skims, Spanx and Vuori).

"As a marketplace of over 5 million creative entrepreneurs, it’s our job to remove barriers for shoppers so they can easily discover and be delighted by our sellers’ special items," Etsy Chief Product and Technology Officer Rafe Colburn said in a separate company post.

The Instant Checkout functionality currently supports single-item purchases, but OpenAI plans to add multi-item carts as an option and expand the service to additional regions.

Merchants pay a fee on purchases, though the service does not come at an additional cost to ChatGPT users, and items with Instant Checkout are not preferred in product results, per OpenAI. However, the tech company said in its announcement that it does consider several factors — such as the enablement of Instant Checkout, quality and price — when ranking merchants that sell the same product.

The new feature is powered by the Agentic Commerce Protocol, which the technology company says was built with Stripe and other partners. In addition to this initial Instant Checkout rollout, OpenAI has open-sourced its Agenetic Commerce Protocol for merchants to start building their own integrations. Businesses can then apply to have their products available to buy through ChatGPT.

"OpenAI is taking its first big step into commerce with Instant Checkout,” Emarketer senior analyst Zak Stambor said in emailed comments. “The feature still has some wrinkles to iron out, but embedding checkout for hundreds of millions of users could turn ChatGPT into a true commerce destination. If OpenAI can streamline the experience, it could challenge Amazon and Google and carve out a lucrative new revenue stream."

The news from OpenAI comes as shoppers turn to AI to ask for product suggestions on anything from everyday essentials to holiday gifts. The impact means that some consumers are shifting away from the search engines retailers have long focused on and changing the nature of their searches to be more complex, even directly on a company’s e-commerce site.

GEO, or generative engine optimization, is the future of SEO, Target’s Vice President of Digital Product Management Ranjeet Bhosale told an audience at ShopTalk Fall 2025 in September.

“It’s not just about giving them the right products. It’s also about how you showcase the product,” Bhosale said. “When they are searching for a summer party, rather than just showcasing tableware they are expecting us to now show party supplies, grilled meat, even sunscreen, and show the breadth of assortment that Target carries in a meaningful fashion.”

Article top image credit: Retrieved from Etsy on September 30, 2025

Stripe’s slower view of agentic commerce

The processing giant, like some other digital commerce specialists, sees agent-enabled shopping evolving at a measured pace.

By: Justin Bachman• Published March 3, 2026

As agentic commerce evolves, Stripe and other payment players anticipate a gradual process for this evolution.

Today, you’re explaining to an AI bot what kind of yoga gear your sister likes and evaluating the options it finds before you handle the payment. But one day, this search-review-pay process will likely happen without you for your sister to receive a gift.

“Like much in AI, agentic commerce suffers from having been overhyped too early in some corners,” Stripe’s co-founders, Patrick Collison and John Collison, wrote in their annual letter, which touched on their views of how agentic shopping will expand gradually across the digital retail world.

“People paint a utopian picture of autonomous agents planning and executing all your commerce by knowing your every whim.”

Instead, they wrote, agentic commerce is likely to morph in “small chunks.”

They categorized these chunks as five levels, layered from the current rudimentary options to a future fifth stage at which an agent — fully aware of your shopping needs and budget — operates without direction. In the Collisons’ ultimate “futuristic vision” example, a child’s back-to-school supplies are purchased and delivered based on the calendar and past budgets.

The second level is more descriptive, telling an agent about a situation for a purchase, as opposed to providing specific attributes, according to the letter. “Today, the industry is hovering on the edge of levels 1 and 2,” they wrote.

The financial potential is large, according to analyst forecasts.

About 81% of consumers are inclined to use agentic commerce tools, potentially affecting $1.3 trillion of spending, according to a survey of 2,532 people in 2025 by Boston Consulting Group. An October McKinsey report on agentic commerce pegged the retail sales opportunity as high as $1 trillion for goods in the U.S. by 2030, and up to $5 trillion globally, not including spending on services.

The same measured approach to agentic commerce is shared by a Stripe-funded startup, Circuit & Chisel, which says it’s “building the foundational technologies that will enable agentic payments and movement around the web.”

The company raised $19.2 million in September to launch ATXP, an agent transaction protocol, to help AI agents navigate the internet and complete transactions, connecting AI and commerce with fewer glitches.

Circuit & Chisel was co-founded by two former Stripe executives – CEO Louis Amira, who was formerly head of crypto and AI partnerships at the larger payments company. David Noel-Romas, who was Stripe’s head of crypto engineering, is Circuit & Chisel’s chief technology officer. They left Stripe in 2025.

“Agents are very likely our target customer moving forwards, which is a thing that got me laughed out of some rooms a year ago, and now sounds way more plausible for a lot more people,” Amira said in an interview.

The New York-based company hopes to become the critical source of tools agentic bots need to improve their function, regardless of whether an agent is from Amazon, Apple, Google or some other provider, Amira said.

“We expect all of them to fight like hell to be the agent that you think about,” he said. “We want Siri or Nigel or Alexa or whatever, to reach for our tools in order to be able to go make things work,” he said, referring to branded AI assistants.

To that end, Circuit & Chisel offers agents email addresses, and is working to provision memory, access to images and payments options as part of its queries to some of the agents now online. “We’re going to keep seeing what they request and just keep adding those things over time,” Amira said.

Amid all the current churn within the AI world, including the various agentic protocols from massive companies like Stripe, Google and OpenAI, the final forms of how agentic commerce will work is still too early to call, Amira said.

“We’re reminded of those few years in the mid-90s when the structure of the internet we use today was hashed out,” the Stripe co-founders wrote, noting the different protocols and providers proffering various approaches.

Said Amira: “Nobody’s really willing to place massive bets on any of this stuff at this point, because it’s just so unclear.”

Article top image credit: Miguel J. Rodriguez Carrillo via Getty Images

Visa, Mastercard reach legal pact with merchants

The legal agreement, if approved by a federal court, could end two decades of litigation between the two biggest U.S. card networks and their merchant clients over credit card interchange fees.

By: Justin Bachman and Lynne Marek• Published Nov. 12, 2025

Visa and Mastercard have agreed to end their longstanding “honor all cards” rule and temporarily lower interchange fees as part of a settlement agreement that could conclude 20 years of litigation over how much merchants pay the card networks and banks.

Under the proposed settlement, merchants will have the right to decline some higher-cost Visa and Mastercard-branded credit cards and will gain new rights to add surcharges for accepting some cards.

The agreement would temporarily cap posted credit interchange rates for five years, including keeping rates for standard consumer cards at 1.25% through the pact's eight-year term, starting with the court's approval. Visa and Mastercard said the settlement also would lower the “combined average effective credit interchange rate by ten basis points” for five years.

A scuttled agreement from 2024 would have reduced fee rates by seven basis points for five years.

The new settlement also calls for a $21 million “merchant education program” to inform the merchants about payment acceptance and cost management.

“After more than 20 years of litigation, Visa and Mastercard have reached a proposed settlement with U.S. merchants of all sizes that would provide meaningful relief, more flexibility and options to control how they accept payments from their customers,” Visa said in an emailed statement.

Mastercard said the proposal will benefit smaller merchants, highlighting a critical reason that a federal judge rejected a prior settlement in June 2024. U.S. District Judge Margo Brodie ruled that that deal did not treat all merchants within the class equitably in terms of their rights to impose surcharges.

The agreement “is the best resolution for all parties, delivering the clarity, flexibility and consumer protections that were sought in this effort,” Mastercard said in a statement. “Smaller merchants will gain in this settlement – more acceptance choices, reduced costs and simplified rules.”

The National Association of Convenience Stores criticized the deal as “more smoke and mirrors” in a statement.

“This proposed settlement endorses business as usual, including by letting Visa and Mastercard increase their own fees without any restraints,” said Lyle Beckwith, the association’s senior vice president of government relations. “That could erase the benefits that this settlement pretends to provide.”

The settlement is subject to approval by Brian Cogan, a federal judge in the Eastern District of New York. Any approval would “occur most likely in late 2026 or early 2027,” Mastercard said in a securities filing.

The marathon class action began in 2005 when merchants sued Visa and Mastercard over alleged antitrust violations with respect to the interchange rates that retailers, restaurateurs and other merchants pay when they accept Visa or Mastercard credit card payments from consumers.

Retailers, including the mega chain Walmart, have been seeking alternatives for years to what they say are the high interchange cost of accepting credit cards.

Under the networks’ “honor all cards” rule, any merchant who chooses to accept a card tied to the Visa or Mastercard network must accept all cards tied to that network, regardless of which bank issued the card or how much interchange fee a card carries.

The rule has meant that a merchant couldn’t refuse a card with a pricier interchange, such as the numerous higher-fee cards that offer consumers travel or hotel loyalty program rewards. Nor could they usually add surcharges for payments with a card that carries a higher interchange cost.

The ability to impose surcharges for higher-fee cards and to decline some costly Visa and Mastercard-branded cards were two key objectives for merchants, Lloyd Constantine, a New York attorney who represents about 40 of the plaintiffs, said in an interview.

About 30 merchants across three plaintiff groups had previously reached independent settlements, including tech giant Amazon, as well as retailers Costco Wholesale and Lowe’s.

The Electronic Payments Coalition, which counts card networks as well as banks and credit unions among its members, supports the latest legal accord. The coalition’s CEO, Richard Hunt, noted that some financial institutions may not be happy with the agreement, given the merchants’ new leeway on which cards they can accept.

“Not everyone in the financial services industry is happy with this agreement which means it’s a good agreement,” he said in an interview.

Still, he noted that the agreement is preferable to any solution from the federal government, which has been threatened in the form of a bill known as the Credit Card Competition Act that was introduced in prior congressional sessions.

Hunt contended that a key benefit of the pact for merchants is allowing more flexibility with respect to surcharging.

Big merchant trade groups, including the National Retail Federation and the Merchant Payments Coalition, criticized the settlement as unsatisfactory.

“This is a bad deal,” said Doug Kantor, who is general counsel for the National Association of Convenience Stores as well as an executive committee member for the Merchants Payments Coalition. “It’s not much different than the deal last year that the judge threw out,” he said in an interview.

Kantor contended that many standard, non-premium cards already have interchange rates lower than the 1.25% cap. Generally, the card networks will still be able to revise their fees to offset any reductions dictated by the agreement, he said.

Overall, he argued that the banks still won’t have sufficient incentive to compete in the credit card marketplace under the new settlement.

Visa and Mastercard faced two trials in 2026 that would have pit the networks against three groups of merchants that had sued over the card swipe fees. The first was scheduled for April 2026 in New York, with a second trial that was set for September in Chicago by a second group, led by delivery service GrubHub.

The proposed settlement speaks to the arms race nature of a new breed of premium, costly cards from banks such as JPMorgan Chase, Capital One Financial and Citigroup that offer an array of enhanced travel and dining perks for affluent customers. Such premium cards carry higher interchange rates, pressuring merchants’ profits.

In September, American Express boosted the annual fee for its Platinum card to $895, months after Chase hiked its Visa-branded Sapphire Reserve card to $795.

The Wall Street Journal first reported news of a pending settlement between the networks and merchants.

Spokespeople for JPMorgan Chase, the biggest U.S. bank, and Wells Fargo declined to comment. Capital One Financial did not respond to an email seeking comment.

Article top image credit: Justin Sullivan via Getty Images

Amazon, Visa team on agentic tools

The e-commerce giant is locking arms with the largest U.S. card network to provide software developers with tools and contacts for creating agentic commerce experiences.

By: Lynne Marek• Published Dec. 3, 2025

Amazon and Visa are joining forces to offer tools and connections in the retailer’s web services marketplace that will let software developers and other companies create agentic commerce experiences, the companies said in a joint press release. They didn’t say when exactly the tools would be available, and a spokesperson didn’t immediately comment on timing.

The e-commerce juggernaut and card network behemoth plan to connect developers “to a growing ecosystem of agentic commerce providers for next-generation reliable and secure payment experiences,” and they emphasized their goal is to allow AI agents to transact “autonomously” on behalf of consumers, according to the release.

Amazon and Visa are also partnering with other companies, including Expedia Group and Intuit, to make the agentic tools available for retail, travel and business-to-business applications, according to the release.

Since at least April, Visa has been talking about creating artificial intelligence-driven agents that can shop on behalf of consumers, noting the arrival of AI-enabled Visa cards that will let the agents make payments. That month, Visa CEO Ryan McInerney told Bloomberg News that consumers would see the tools in the market “soon,” without providing a specific timeline. The card network talked about protocols for agentic shopping again in October.

Visa Chief Financial Officer Chris Suh explained at an investor conference in November how Visa is investing to compete in the agentic ecosystem. “The pace of innovation, as we can all see, is very fast, perhaps even accelerating,” Suh said at the KBW Fintech Payments Conference. “Some of the topics of late, around things like stablecoin and agentic, clearly, there’s a lot of interest and innovation and investment happening in Visa, and also in the entire ecosystem.”

Visa and Amazon are teaming up as players race to embrace the promise of digital agents that will shop on behalf of consumers, tapping artificial intelligence to make decisions about purchases and payments based on initial commands.

Digital payments pioneer PayPal Holdings, processing giant Fiserv, digital payments startup Stripe and Visa rival Mastercard are among the many companies seeking to make bot-shopping a reality for consumers.

The latest announcement comes as Amazon has become embroiled in litigation over how such agents operate on its marketplace. In November, the online retailer sued artificial intelligence company Perplexity in federal court over its use of AI assistants in Amazon’s retail sphere.

While some companies have said they’re testing AI-driven shopping tools, including payments processor Worldpay, there are currently few real-life use cases in the marketplace.

Some professionals have noted there are numerous issues yet to be resolved for such commerce, including what happens when such agents go haywire and purchase the wrong items, requiring returns and refunds. Such outstanding issues present risks for use of the new shopping tools, they say.

Article top image credit: Alamy

Klarna counts on retailers for growth

The buy now, pay later giant says the availability of its services at retailers such as Walmart and Macy’s correlates strongly to future growth.

By: Justin Bachman• Published Sept. 11, 2025

Klarna Group wants to make its buy now, pay later option "ubiquitous" at the retail checkout as a primary engine for future growth, the company’s chief commercial officer said in September.

“Our aspiration is to be ubiquitous at the checkout, and what that drives is actually a habitual behavior of, ‘I see Klarna, it's regular, I can use it more often,’” Chief Commercial Officer David Sykes said in an interview a day before the company’s initial public stock offering.

One area of retail progress: Klarna will debut its short-term loans at Walmart in September, a company spokesperson said. That lending debut comes six months after the company announced that it had wrested the largest U.S. retailer away from BNPL rival Affirm Holdings.

Klarna is being incorporated into Walmart’s OnePay digital payments app that shoppers can use at their checkout in stores and online. Loan repayments will range up to three years, managed via the OnePay app, the companies said in March announcing their partnership.

Klarna’s business began in Sweden, spread across Europe and has spurred a worldwide trend over the past decade, inspiring a batch of BNPL companies, including several U.S. rivals such as Affirm, Block’s Afterpay and Sezzle.

An Affirm spokesperson declined to comment about when the Walmart partnership would conclude. In August, Affirm said in its quarterly shareholder letter that it expects to “substantially transition” from Walmart by its fiscal second quarter of 2026 as the retailer adds the exclusive tie to Klarna.

In May, Costco Wholesale said it would add Affirm as a BNPL option for sales of $500 or more made at its online store; although customers can also use Klarna through Apple’s digital wallet. Affirm has also been the primary BNPL option at Amazon since 2021 for purchases over $50 although that relationship is no longer exclusive.

London-based Klarna counts 790,000 merchants and 111 million consumers in 26 countries, the company said in August in releasing quarterly income results ahead of its initial public offering. The number of shoppers using the payment method jumped 31% for the second quarter, compared to the year-earlier period, the company said. The U.S. is the company’s largest market, according to its financial release.

For its long-awaited IPO, Klarna offered 34.3 million shares priced at $40. The company’s stock began trading Sept. 10 on the New York Stock Exchange.

Klarna views retail transactions as structured like a pyramid, with abundant lower-value purchases – tennis shoes, cosmetics and Uber – at the base and far fewer high-value transactions at the top, Sykes said. Klarna favors the higher volume approach.

“Some of our competitors start higher up on the pyramid,” he said. “They start with expensive electronics, expensive mattresses and all the rest. The challenge with that is there’s just less (purchasing) of them.”

The higher-end approach could have described U.S. rival Affirm in the past. At one point after the start of the COVID-19 pandemic, the maker of $1,000-plus Peloton stationary bikes was Affirm’s biggest client and accounted for a significant portion of its sales.

Despite its recent Walmart win supplanting Affirm, Sykes noted that retailers can offer multiple BNPL providers and said that attracting repeat users matters far more than snagging a spot on a retailer’s list of checkout options.

Target, for example, accepts payments from a half dozen BNPL providers including Klarna for online and mobile app purchases, while numerous retailers such as Best Buy, Macy’s and Dick’s Sporting Goods allow customers to use multiple BNPL providers for payment.

Klarna can be used for payment at dozens of merchants, including Airbnb, eBay, Foot Locker, Lowe’s and Neiman Marcus.

“I think we are totally agnostic as to whether a partner has one or multiple options, just to be totally frank,” Sykes said. Over the past 20 years, Klarna has learned that “it doesn’t matter what you do” beyond becoming the shopper’s first choice, he said.

“All that matters is consumer preference,” Sykes said. “Customers have to want to press that button. So when I think about where we spend most of our time and energy and effort, it’s giving the end consumer a heap of reasons to click that Klarna button.”

Article top image credit: Courtesy of Klarna Group

The biggest payment trends in retail

Retailers are thinking through the best way to streamline and incorporate payment options as a way to capture, delight and retain shoppers. Millennial and Gen Z shoppers are leading the way when it comes to contactless payment adoption, and retailers are rolling out options like buy now, pay later and checkout-free capabilities.

included in this trendline

ChatGPT lets shoppers buy products within the platform

Checkout-free payments may yet rise

Gap Inc. teams up with Klarna on flexible payments

Our Trendlines go deep on the biggest trends. These special reports, produced by our team of award-winning journalists, help business leaders understand how their industries are changing.